Time is the single most important constraint of the universe, yet we too often forget the variable, T, in our economic models.

Time is required for planning. In my current job, things have been going really well. Over the past year, much of my time went into formulating a plan for where I would like to be. Now, it feels like I’m where I want to be. The question then becomes how do I execute better right here, right now?

Planning is essential. People have workout plans, moving plans, birthday plans, cooking plans. But many people don’t create plans for their lives. They should. When I played chess, there was a common adage that “a bad plan is better than no plan.” I wanted to lay out a plan for how to maximize my output and create clarity around my path forward. That was the original intent of this essay.

But with every plan I wanted to create, I kept running into the constraint of time. Time is a central variable to every plan, instruction manual, etc. While I was writing notes for myself, they turned into a much longer template for this essay on time.

The Past and Present

In order to plan for the future, it is important to know your history and present state. Who were you? Who are you now? Can you connect the dots to project a forward looking trajectory? So I asked the question, what are my strengths, weaknesses, and individual characteristics. 5’11, 23.9178 years old, hyper-ambitious, intellectually curious, dashingly handsome… Sparing the details, I deeply believe that the person I am today can accomplish whatever I set my mind to.

Set your time horizon. The median male lives ~73 years, so we can assume I’ve got another fifty in me. That’s a lot of time, and yet not much at all.

Then identify in exact detail what end goal you have for 5, 10, 25, 50 years and bridge the gap between the two states through concerted effort.

Interests

What you do in between is what you need to do and want to do to accomplish your goals. What are my interests? Why are we interested in anything? After belaboring this question across several essays, I’ve determined that my interests lie in their ability to provide me opportunities for growth and striving.

I am interested in finance & technology, because money runs the world, and technology changes it. These are also areas of leverage in capitalism, which I will get to later.

In this world we were born into, money is the proxy for value and growth. Understanding the proxy isn’t perfect, I will still measure growth in money and profits. Money runs the world.

Capital Accumulation

Unless you are stealing, the trodden path to capital accumulation comes from providing X amount of value and capturing Y% of the value through the transaction(s). You can do this yourself directly or through the ownership of an organization, network, business, etc. that provides the value.

Time as a Variable

Time is extremely important in business. It is an often forgotten variable in the equation of value capture. You can build your company with many specific goals in mind. One is to purposefully engineer your company in a way to maximize velocity.

Time is important for 3 reasons. One is strategic and the other two can be thought of as optimizing a variable in the capture of value:

Business Strategy (strategic)

Speed of execution and momentum are powerful differentiators as a business strategy in shipping new products, pivoting, capturing market share when network effects matter, etc. Travis May, CEO of Shaper Capital, says that businesses often don’t operate near the efficient frontier where speed trades off with quality, budget, and other constraints.

“Strategy, its high-church theologians insist, is about outflanking competitors with big plays that yield long-term “rents” from a sustainable advantage. It is questionable whether this proposition is itself sustainable. Strategy involves a lot more and also a lot less. The competitive scriptures almost systematically ignore the importance of hustle and energy.” - Harvard Business Review: Note: Read Hustle as a Strategy - HBR

This is also why software has captured my attention, it is fast, and not in a “get rich quick” kind of way. Coming from the world of biotech, if it de-facto takes years to get to market and regulatory bodies punish you every step of the way with extremely high upfront R&D costs, the barriers, drag and friction to success are too high.

“I think there is something about software itself that's very, very powerful. Software has these incredible economies of scale - these low marginal costs - and there is something about the world of bits as opposed to the world of atoms where you can often get very fast adoption and fast adoption is critical to capturing and taking over markets. Because even if you have a small market, if the adoption rate is too slow there'll be enough time for other people to enter that market and compete with you whereas if you have a small to midsize market and have a fast adoption rate, you can take over the market.” - Peter Thiel.

Time to success is speeding up. This software-margin enabled high-velocity company blitzscaling is a large factor in how Time to market is speeding up. You used to hear war stories of the older generation about how they painstakingly built their company over a period of 50 years. That is now 5 (still painstaking) years in software.

In addition to accomplishing things faster. If you put more hours in per day, you will accomplish more in aggregate, despite less being accomplished on the margin. I was never a smart kid or the best in school, but I did pretty well for myself by simply outworking the competition.

For inspiration, here are also remarkable examples of people quickly accomplishing ambitious things together. You wouldn’t want to compete with these teams. Fast - Patrick Collison. The Manhattan Project took 3 years. What if it took 10?

Captured Value Per Time Unit

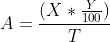

Make more money in less time. If it takes one salesman 4 hours to source and close a customer and you cut time in half you are doubling the efficiency of your salesman. If you then allow him to run 2x the prospects in parallel, you are quadrupling the net new bookings. It is not this simple in practice, but the idea that if you multiply the amount of sales done per quarter / per annum is powerful. In Figure 1 below, this is equivalent to dividing T by 4. You are quadrupling revenue and making a leaner business per unit of time.

Figure 1: To create some logic around this concept, the following formula represents the value captured per unit of time.

A = Value Captured Per Time Unit

X = Value Captured

Y (0 -100) = Portion of Value Captured

T = Time Unit

Compounding Value

Arrive sooner. What if we harnessed electricity 100 years earlier? What would society look like today?

The majority of a company’s payoff comes after it has reached a more mature state in the future. When valuing a company, often over 70% of the company’s value comes from its terminal value in a discounted cash flow analysis. This is when it has topped out in growth, generates the most cash flows, and is expected to operate into perpetuity.

X and Y are not constants. Profits increase exponentially. We should both expect and push extremely hard to increase the slope of the growth curve and value we provide as revenue scales / product becomes more useful. We should also expect margins to widen with economies of scale. By scaling a business 2x as fast, we are able to hit our terminal value in 5 years vs 10 years. Referring to Figure 2 here.

Figure 2: To be honest, I haven’t taken calculus since high school, and I don’t even remember if I’m doing this correctly, but this is supposed to represent the integral and cumulative value captured over T time period.

C = Cumulative Value Captured Over Time in Period

Multiply your value. Imagine that the business in Figure 3 is sold at year 2.5 at a 10x revenue multiple for $50 million. If the company had arrived at year 5 sales in half the time, the company would be selling at a 10x revenue multiple for $250 million. Do not underestimate the value of compounding.

Figure 3: The actual value captured over time depends on the time horizon

The three forces work together. What’s more important than the principle of each of these separately is the value of the three combined. If your competitive speed allows you to gobble up market share and ship new products to expand, make 4x the revenue per salesman/year, and the speed of your business means you get 5 years of work done in a 2.5 year period, you will be so far ahead of your competition that they will never catch up to you.

Figure 4: The same principles that apply to physics apply to growing your business. You should be accelerating constantly, increasing the speed of your organization, and the distance you reach will compound over years. An even 1% increase in acceleration per year will pay massive dividends.

Profit

Now we understand the importance of time in compounding profit, essentially minimizing the value of variable T.

Next, we should dig into how exactly to make money in each unit of time. My findings so far is that making money is easy. However, making a lot of money is hard and ROI becomes harder to find with scale. You need leverage to accomplish more than what you are able to do with your humanly time, essentially maximizing variables X and Y.

The three major buckets of leverage I explore are leverage over people, assets, and financial leverage (these buckets are blurry and could probably be reworked). In each of these, there are inputs and there are outputs.

Both can be thought of as aiming for a high Return on Investment. Both can also be seen as lowering inputs and increasing outputs. Both can be thought of as maximizing margins. They’re all interconnected and maybe I will even propose a new economic term for the intersection of the two one day.

Leverage of People

Hire people to add more time to your day. Because your time is limited, and your focus is valuable, you should pay other people money to conduct operations in your place. This shouldn’t be thought of as pure leverage. Ideally both transactors, the employer and employee benefit from the working relationship.

This is a required step in scaling yourself. This could be its own essay as well. It is not possible to be the best at everything. At some point in time you will need to hire someone to accomplish something that you are simply not able to alone. At the same time, developing skills and increasing the value of your own time is important to know where to invest your time and resources. You should learn to develop these forms of trust and relationships from the beginning so that your management strategy can scale.

In order for this to function, ideally employee wage < present value of profits associated with the person.

Leverage of Assets

If you own an asset that either stores value or generates cash flows, it has intrinsic value that is not directly tied to your time. An example would be a golden goose that lays a golden egg every day. This can also be leverage of technology to compete better.

You can buy these assets at a discount to their intrinsic value, use the passive income to accumulate additional assets, create these assets with your own time, etc. This pattern is also found in the next category.

Leverage of Equity

You invest money in an ongoing concern/business. This can almost be thought of as a combination of 1 & 2. You are buying or building a living and breathing corporate organization that functions as a machine of moving pieces of people, networks, and assets. Labor/investment as an input and profit/desired change as an output.

Each business has their own unique combination of inputs and outputs that best positions it to provide value to their customers and then secure a portion of it.

Berkshire Hathaway does this through investment alone, Elon does it through company building alone. Value investment is just value arbitrage. Buying good companies at a cheap price. The alternative is to build a great company from scratch. Which should you do? I argue there is a tradeoff.

Time vs Resources Tradeoff

I equate the tradeoff of output relative to labor and investment in the same way that Einstein outlines The Theory of Special Relativity, which explains how energy and mass are interrelated. It outlines the formula e=mc^2, which states that energy is equivalent to mass times the speed of light squared.

Similarly, it seems to me that just like a small amount of mass can produce a huge amount of energy, a small amount of time and labor (your work) can lead to a significant amount of profit, especially when multiplied by smart investment strategies (like the speed of light squared in the equation). Larger mass generally equates to higher energy. Larger starting investment equates to more profit/growth. Not a perfect analogy, especially since c is supposed to be constant.

Which should you do then? Should you invest in assets and people? Should you invest in businesses? Should you create your own? It depends.

If the goal of this exercise is purely profit-driven and to maximize ROI, then …. It also depends. It depends on who you are, what you have, what you know, who you know, and the current state of the world. It depends on the value of your time.

Value of Time from Financial Leverage

Someone who has $10,000,000 can invest that money and make $500,000/year without working. They are using leverage over their capital and taking up a low salary job would not be worthy of their time.

Value of Time From Work Exerted Upon a System

If you have no resources to invest, your only asset is yourself. If you are flat broke with no skills, you need to work an unskilled job and invest in yourself.

Someone who has $0 in the bank has Zero financial leverage. How do they create value out of thin air? This is the problem that all us broke-ass mortals have to face. Assuming we have no other resources, the only way that they can accumulate capital is by using our time to create value in the world and capture it or to sell our time itself to a company for value we provide to them.

If you have leverage over a network of people, a skill set, or some other resource, that increases the value of your time and ability to leverage these resources to earn a profit. But you will still be deriving income from other forms of leverage.

Probably within this time to earnings matrix, there is a breakdown of the leverage you can get from different jobs. As a general rule, it is better to be paid in equity at a company you contribute greatly to the success of; however, lawyers don't do too poorly billing hourly. You just need to create X value and capture Y% of it. However, as a human being, you can only scale yourself so far.

Unskilled hourly employee

Salary

Skilled Salary

Commission

Leading a Team

Equity in the Company

Efficient Markets

This is probably why people say making your first $1,000,000 is always the hardest. To build yourself up from a worthless human with no skills and no network and no cash in the bank to a net worth of $1,000,000 is the early part of the growth curve and is excruciatingly painful. This is no-man’s land, because you don’t really even have access to financial leverage. The ROI on a $200,000 investment to support your life and reinvest the surplus is high. You would need to return 25% YOY to regularly bring in $50,000/year pre-tax. Even Wall Street’s best can’t squeeze much greater than the market average of 8%/year from the market.

This is because the public stock market is mostly efficient. It is difficult to gain a high Return on Investment. So extracting Y% is more difficult because it is difficult to find mispricings. Warren Buffet continues to sit on a pile of cash. This is also in large part due to the scale of Berkshire Hathaway. It’s hard to find enough good deals. Warren guarantees he could return 50% if he was only investing ~$1,000,000.

In fact, most markets are efficient now. Starting from the most liquid and efficient mega-cap companies downstream through private equity investors LBOs to growth equity, and the recent inundation of money into venture capital. Doug Leone of Sequoia recently said in a podcast that venture has permanently shifted from a high margin cottage industry to a low margin mainstream business. It's going through a parallel evolution that private equity/buyouts went through in the 90s/2000s. You now have "megafund" venture shops that are raising fund sizes on par with PE, which was unheard of a decade ago. For the last decade, mid to late stage growth equity has been where the easiest alpha was - put a bunch of money into a basket of SaaS startups at Series B/C/D, and like magic they would IPO in a few years at a 5-10x MOIC. Now it's arguably the seed stage, where all the money and deals are crowding now. VC will have its up and down cycles, but it is forever now a true institutional asset class, with tons of competition and decreasing alpha. PE in the 90s up to the early 2000s for example was much less competitive and institutional than it is today. Now it's brutally hard to build a career in buyouts, with more investors with more dry powder chasing the same deals. Still achievable of course, but the degree of difficulty and level of competition is an order of magnitude higher. Venture is undergoing the same dynamic. I don't know if it's honestly a good place to build a career anymore. It's certainly a lot harder to advance and generate returns now and going forward.

Even software has become pretty efficient. Where there is a problem, there is probably a software solution.

The one counter-point I have to the fact that saturated markets are harder to win is that they are the industries that often have the most capital available for capture.

Find inefficient markets to capture more value.

Inefficient Markets

In theory, any market could be inefficient. Technology is just interesting because it can catalyze a seismic change that disrupts an efficient market. However, you can also invest based on socio-political events and the likes. It feels like while other events can change the course of humanity, they are mostly moral questions.

Most markets oscillate between inefficient and efficient due to new technology. AI and crypto are going to shake things up in a similar but different way that the internet and software did. Crypto is version 2 of the techno-libertarian internet movement and the return of monetary governance to private markets. AI is software 2.0 and enables us to better work with computers. It’s almost like software went from analog to digital, only to go back to digitally enabled analog systems. I imagine this as a computer that you speak to and it understands you, rather than breaking the entire system if there is a missing 0 or 1 in the underlying machine language. AI is also much more than this. Just as there slowly became a playbook for value investing, then software, the same will occur for these technologies.

Zero to One is what really enabled me to come to this realization. I believe that the last frontier for inefficient markets are the markets that do not exist yet. Technological development is accelerating and sure as hell will not stop. This is the next stage of human evolution. Not because it is morally right, but because it wins.

Even when these markets are small, they are growing fast. So you need to act fast to wedge yourself in and expand. Time matters.

Zero to One

For this reason, Zero to One is way ahead of its time and will go down as the piece that represents this generational tectonic shift. I will not do the injustice of putting Thiel’s words in my own poor writing style. Read it if you have not.

Also, you don’t necessarily need to go from 0 to 1, or 1 to 2, or 10 to 100, or 1,000,000 to n. Each of these are different opportunities and require different skill sets for different inefficiencies.

What I will say is that if you are the person who owns the machine, rather than an agent of it, you can put the right resources and people in place to make the machine run optimally. I don’t know what this role in a company is, but it is what I want to do. CEO?

Company Formation VCs

Venture capital is going through a phase of its evolution. The biggest generalist VCs become a stamp/commodity, the few winners take all, and specialized VCs take hold as they are more skilled in their area of expertise at lead generation and investment decisions. In a lot of ways, VCs have become commoditized “money providers.”

Use the “but-for test” to see which party provides the most value to society. The but-for test is a test commonly used in both tort law and criminal law to determine actual causation. These companies could have been started without the VCs, but could not have been started “but for” the founders. When in any startup, you quickly realize that the bottleneck of progress is just having people who actually build the damn thing. Be the person who actually builds the damn thing.

Y Combinator essentially acts as a fish net/index fund/esteemed university for people who actually build the damn thing. It was essentially a realization that the engineers are the people who actually have the value to create the software companies. They are a really interesting business model that I expect to exist for a long time, similar to universities. But accelerators are passive. They help the founder to raise. However, just as a student graduates from college, they can graduate from Y Combinator. By the founder’s second company, giving up 7% of a founder’s company may no longer make sense for the YC stamp/network. Or maybe YC will forever play an important role in many companies’ formation.

They also say that the best VCs have run companies in the past. So I think it could make sense that the next generation of VCs are both a founder and investor. They know their markets. They can create, lead, and invest in the next generation of organizations that will go on to “shape” (Shaper Capital) those industries.

Venture Studios aren’t even the right term. These are investors and operators who specialize in going from 0 to 1. Still trying to think of a better name. If you look at Founders Fund today, they are who do this. They invest in companies, but also start them if they see a problem or inefficient market that has not been solved.

I wonder if we will see vertically integrated funds. Creating the company, leading its rounds, and then reinvesting its dividends across many companies at scale.

What investment strategy comes before company formation and 0-1? There is nothing before 0. The only thing I can think of would be an investor like Flagship Pioneering, who forms the company after they have already incubated breakthrough science through experimentation. So engineers/scientists keep winning?

This may actually be the final phase of great investment companies. Perhaps it will continually fragment. Some will win for a time, then lose, and others will take their place. The cycle of life.

What I do know, however, is that technology is the infinite frontier. Until computers have replaced us, there will never be a lack of problems in society that humans can exercise their time and agency upon to solve.

One of the great things that I am starting to learn is don’t be a commodity. This goes hand in hand with the idea that whatever it is you do, make sure it provides value and do it the best in the world. Do it so well that you are playing your own game and no one will ever catch up with you.

Company formation is also a messy process. I think you can commoditize a founder’s playbook and do it at scale, so that the only thing left is to find new problems and continue to execute better.

We have the playbook for software for the most part. It probably makes sense to begin drafting that up more explicitly. And it also probably makes sense to start drafting the playbook for starting an AI company more explicitly.

The New Playbook

I am yet to see what the strategy will be yet, but I expect that the strategy of these new formation VCs will differ widely depending on the firm. It will likely be like an entrepreneur with significant company formation experience doing it without having to think about raising capital. So it will be like the investment process has become commoditized and done in-house.

Most traditional VCs without experience building companies will not be able to effectively run a venture studio. In order to become the type of person who would run a company formation VC well, you first need to become a strong individual contributor and learn how to build a company. You need to learn how to do it so you can do it multiple times at scale.

Each will have a different culture. Each will have a different strategy. Each will be knowledgeable in its own domain.

Conclusion

Create a plan for your future. If you want to accumulate capital, you will need to add value. Do not just participate in the market, work within the constraints of time and resources to actively shape it.